According to the Shipping Industry Network, Clarksons stated that the new shipbuilding market is entering a "super cycle" with a surge of orders, scarce shipyards, and high prices for new shipbuilding. The driving force for further growth is convincing.

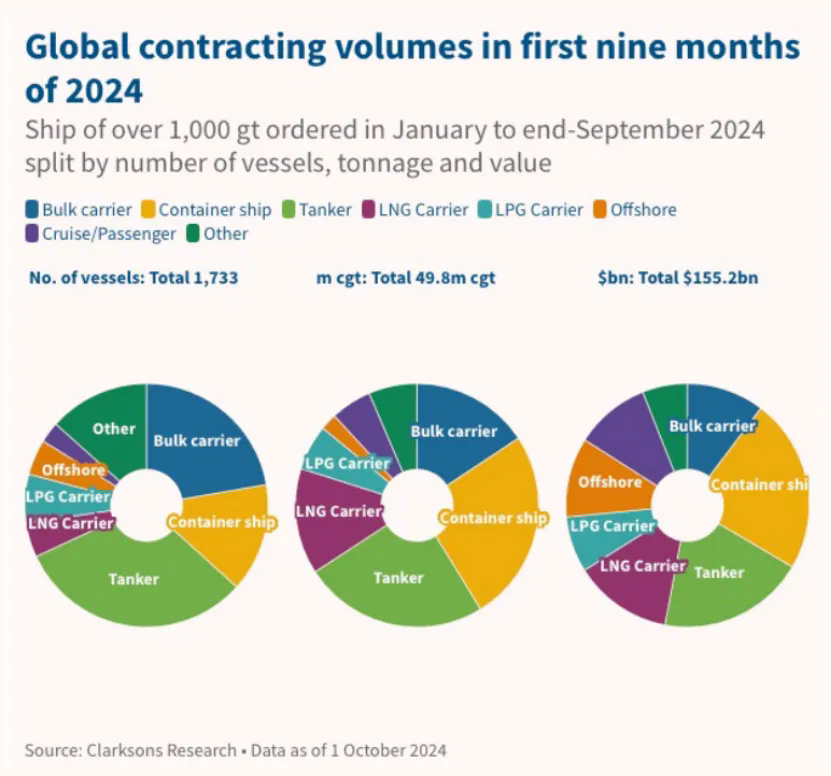

Clarksons data shows that in the first three quarters of 2024, new shipbuilding orders reached 1733 vessels, slightly below 50 million corrected gross tons (CGT) or 94 million gross tons, valued at approximately $155.2 billion.

Clarksons Research's Global Managing Director Stephen Gordon stated that this is the strongest and most active new shipbuilding market since the "supercycle" of 2007 and 2008.

Clarksons predicts that by the end of this year, orders will climb to approximately 2200 vessels, with a total tonnage of around 115 million, surpassing the levels of 2021.

Stephen Gordon stated that orders for container ships and LNG carriers have continued to increase this year, while oil tankers have also been active. Orders for bulk carriers have remained stable, and cruise ship orders have also recovered. However, the proportion of orders for oil tankers and bulk carriers in the fleet is still at a historical low.

Stephen Gordon pointed out that the strong cash flow of the shipping industry and the demand for fleet renewal and decarbonization are the key driving forces of this round of new shipbuilding market.

He stated that ClarkSea (Shipping Composite Index - covering rental rates for four shipping segments) showed an average of over $25000 per day in the first three quarters of this year, which is 47% higher than the average since 1990 and 35% higher than the average level in the past decade, indicating a significant inflow of cash into the entire shipping industry.

But compared to the previous cycle, the total order volume is still 35% lower, and since the last shipbuilding peak in 2008, the world fleet has doubled.

There are subtle differences and driving factors in each segmented market

He said that LNG ships are being ordered to meet the demands of new projects, and for container ships, the Red Sea crisis has led the market to believe that greater "redundancy" is needed to flexibly respond to supply chain disruptions.

The number of cruise passengers rebounded to 35 million after the pandemic, higher than pre pandemic levels, prompting the market to order large vessels - which is very encouraging for the European shipbuilding industry.

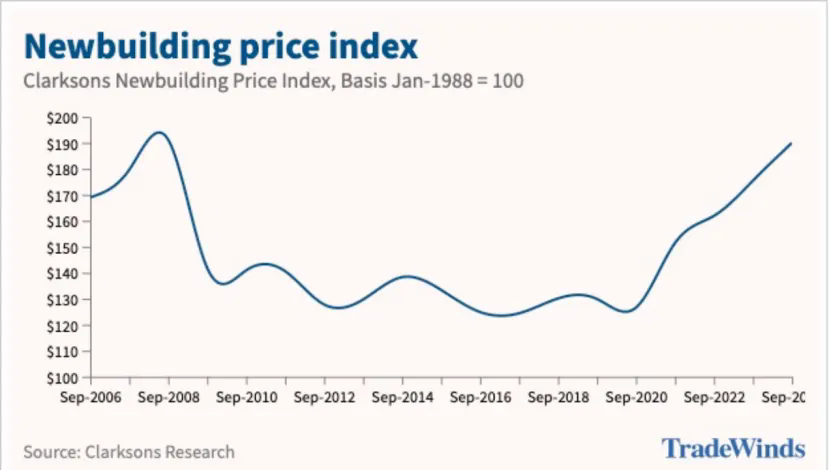

The Clarksons New Shipbuilding Price Index has risen by 45% since the beginning of 2021.

Stephen Gordon stated that since the beginning of this year, the price of new shipbuilding has increased by 5% to 6%, but the rate of increase has slowed down.

The cost base of the shipbuilding industry has increased, highlighting the rise in labor costs. However, strong cross industry demand and forward orders from shipyards have consistently supported new shipbuilding prices.

He pointed out that shipbuilding capacity increased again after plummeting by 40% from 2010 to 2020.

The market tells us that additional shipbuilding capacity is needed to advance fleet renewal plans and decarbonization

He said that over 75% of the capacity expansion is concentrated in China. More than half of them are expansions of existing shipyards, while the rest are restarts of facilities that have already been closed or used for other purposes.

He said that unlike the previous cycle, there are almost no new shipyards built now, and there is not much growth in other parts of the world.

Although the global order volume is 35% lower than in 2008, China's order volume is already at its highest level in history.

Overall, Clarksons expects to deliver over 40 million CGT this year and next year, up from approximately 30 million CGT in 2020.

Looking ahead, Stephen Gordon stated that $5.5 trillion in new shipbuilding will be needed by 2050, primarily for fleet renewal and decarbonization, but also for trade growth - which is different from the situation at the beginning of the 21st century when trade growth was the main driver of shipbuilding industry growth.

Clarksons is "very optimistic" about gas ships such as LNG, LPG, ammonia, and carbon dioxide, and remains optimistic about the floating production, storage, and offloading (FPSO) industry.

He said, "I am optimistic about the overall market, but the uncertainty and risks are also very real - many of which are geopolitical factors, including the Red Sea crisis. The increasingly complex trade outlook has added a certain degree of uncertainty to certain segmented markets

Please enter the keywords of the content you want to search for to start the search.